In the past few years, there has been a lot of hype around blockchain. Investors have been blindly investing exuberant amounts of money without clearly understanding the viability of blockchain based business models.

VC funding for blockchain start-ups has consistently grown, with venture investment reaching around $1 billion in 2017 (and likely to be more than double that amount in 2018). Initial coin offerings (ICOs), the blockchain-based fundraising model involving the sale of cryptocurrency tokens in a new venture, have also grown exponentially with more than $5 billion raised through ICOs in 2017. Even executives of long established companies have become eager to jump on the band wagon of being blockchain-enabled.

While it is a very useful technology, blockchain is not a solution to every problem. In many cases current systems are better than blockchain as they may require less capital expenditure, pose fewer security risks, allow for faster transaction processing, or consume less energy to verify transactions. Many startups are also trying to create blockchain based solutions for problems that can be solved better without blockchain. According to Deloitte, 92% of the 26,000 blockchain-based projects created since 2016 are now dead.

Wouldn’t it be great if there was a way to determine whether your blockchain based startup idea is viable?

To help you do this, we will now look at the four steps involved in the creation of any blockchain-based startup:

- Identifying a use case

- Building a proof of concept

- Conducting a field trial

- Implementing the solution at scale

1. Identifying a use case

Even though most startups take a fail-fast learn-fast approach, answering two simple questions can help you avoid some known land mines and save you a lot of time and effort.

Q1: Is it a problem worth solving?

You need to do some market research and a few back-of-the-envelope calculations to determine the size of the target market, whether there is sufficient demand for the solution, and how much potential customers may be willing to pay.

Q2: Will replacing an existing solution with you blockchain-based solution deliver significant incremental benefits?

Even if your new solution is objectively superior, will customers be willing to pay for it? No client will want to undertake a major overhaul to their existing systems just to save pennies on the dollar.

Even though it sounds obvious, most startups fail to consider this important question. This may be one reason why so many startups fail. They created a product or service which solved a problem that no body cared enough about.

Segway is a classic example of such a product. The upright scooter was supposed to revolutionize transportation but all it did was make riders looks silly and self-satisfied. It was a solution in search of a problem, just like many blockchain based startups today.

Hence, it is important for startups to think critically about this question, do some basic math, and proceed further only if the idea clears this initial feasibility test.

Blockchain’s core advantages are decentralization, cryptographic security, transparency, and immutability. It allows information to be verified and value to be exchanged without having to rely on a third-party authority. As a result, blockchain is most likely to deliver value in the following cases:

- Disintermediation

- Data security

- Decentralized data

- Multiple stakeholder environments

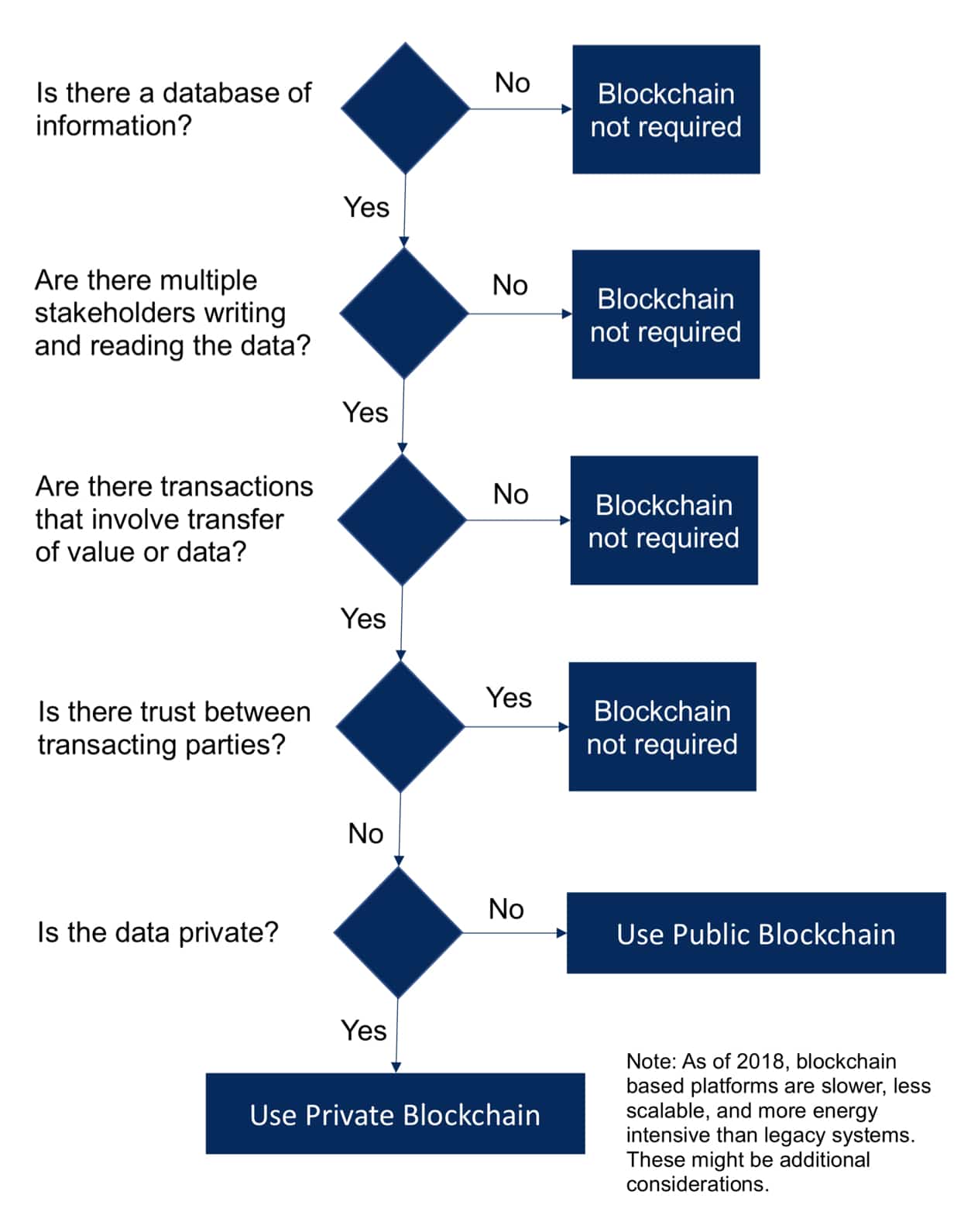

The following flowchart can be used to determine whether blockchain is the right tool for the job.

Figure 1 – Screening problems to see if blockchain is a suitable solution

Depending on the needs of stakeholders, startups have to figure out whether to go for a private permissioned or public blockchain architecture.

This first stage of identifying use cases does not require any major investments but is key to the success of your startup.

2. Building a proof of concept

Once a use case has been identified, it should be validated by building a proof of concept (sometimes called a “minimum viable product”). This step involves building a system to collect data and the blockchain infrastructure required to process it. This phase may require substantial funding as it involves experimentation and testing. Teams need to be agile and ready to adapt as new information is received.

3. Conducting a field trial

After building a functional product, the next step is to run a test pilot. This involves using real world data but in a controlled environment. For example, in 2016, New York based startup LO3 Energy ran a test pilot to create a micro-power grid in Brooklyn, allowing neighbours to buy and sell locally produced solar power using a blockchain platform.

4. Implementing the solution at scale

Before scaling, you should make sure that all of your intellectual property is protected. Trademarks and patents need to applied for. Startups should partner with major players in the industry in order to implement the solution. The goal should not be to completely replace existing players but to work with them to transform and improve the industry.

To conclude

Blockchain has the potential to revolutionise the way that value is exchanged and data is transferred, and this will transform a wide range of industries. But, it is worth keeping in mind that not every problem can be solved using blockchain. The technology has limitations in terms of transaction speed, the volume of transactions it can support and the scale at which it can be implemented. Also, the development platforms are still very rudimentary making it a challenge to create an error free blockchain infrastructure. Before committing time and money, startups need to ensure that the costs of implementing the technology do not outweigh the benefits.

Mudassar Shaikh is an engineer at heart, management consultant by profession, entrepreneur by spirit, and student by essence. He is passionate about enabling organizations to develop new technologies and make them accessible to the masses, positively impacting the life of many and pushing the human race forward.

Image: Pixabay